Fig 1: shows an eXtra store, Saudi Arabia’s leading electronic retail. Source: alroyya.com

Retail industry is the part of the economy, involved in selling finished products to the end users. Retail shops could be found in wide range of formats, ranging from large hyper markets and department stores, to small convenience stores and general stores. It primarily includes six sub categories: - food & general retail, fashion apparels, fast food restaurants, fast manufacturing consumer goods (fmcg), luxury products and electronic appliances & consumer durables.

All across the globe, both in the developed as well as developing world, retail industry plays a pivotal role in the national economies. It has a wide range of direct as well as indirect economic significance- ranging from mass level employment generation (both urban and rural) to bringing, speed and efficiency into the entire supply chain system.

The given report intents, comparing retail sectors Malaysia and Saudi Arabia; one an emerging economy and a constitutional monarchy from South East Asia and other an oil rich Islamic Monarchy from the Gulf. Both the nation, share similarities across various socio-cultural as well as demographic parameter. Hence provide a good case to do comparative analysis. They will be compared across following parameters- economics, retail industry outlook, policy frame work, tourism, demographics and transportation.

Economics, demographics & infrastructure

The following part compares Malaysia and Saudi Arabia, across few of the general economic, demographic and infra structure related parameters.

Fig 1: shows the GDP growth rate of Malaysia and Saudi Arabia vis- a-vis, world’s growth rate.

Table 1: compares Malaysia and Saudi Arabia across various economic parameters. Source: World Bank

Table 2: compares Malaysia and Saudi Arabia across parameters related to infrastructure. Source: World Bank.

Retail industry outlook

Malaysia

Malaysia, an upper middle income country according to World Bank, enjoys a robust and growing retail sectors. According to Business Monitor International, total retail sales in Malaysia were estimated at US $ 33 billion, in 2009. Like other Asian countries it has penchant for gigantic malls and hypermarkets and is dominated by players such as Giant (domestic), Tesco (UK) and Care four (France). The retail sector in Malaysia is fueled by large proportion urbanized middle class (50% of the population) with high disposable income; a large proportion of youth (42% aged between 10 and 34, as on 2008) and high tourist arrival. Tourism accounts for 30% of retail consumption in Malaysia. (RECON, 2008)

Fig 2: shows the growth in retail sales vis-a-vis GDP growth rate for 2010. Source: Thestaronline.com

Fig 3: shows the number of outlet and total sales for major retailer in Malaysia for 2009. Source: Malaysia retail annual report, USDA Foreign Network.

Saudi Arabia

Saudi Arabia is the biggest Gulf country and the biggest economy in the Middle East and North Africa region (MENA) region. The region is marked by growth in retail space, young demographics, high tourist arrival and change of role of women in social sphere. Saudi Arabia, the biggest and one of the freest economies in the region, is considered as one of the most fertile market for the retail industry. Rapidly growing population, brand conscious young demographics (45 percentage of population aged 20-44) and high level of disposable income will be key drivers for the industry, in the kingdom. After oil, banking and telecom; retail is the fourth largest industry in the country, both in terms of number of, establishments as well as employees. It earned a total of US $ 55 billion, from retail sales in 2008, up from US $ 37 billion in 2004. (PR Log, 2009) The market is dominated by small retail stores, though big retailers, both domestic and international players, are trying to up their ante in the much fragmented retail industry.

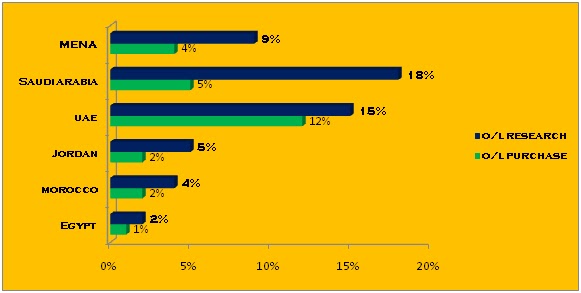

Table 3: shows values for various retail industry related parameters. Source: JONES LANG LASALLE, AMEinfo.com

Fig 4: shows the retail sales of Saudi Arabia, in billion US $, over the last few years. Source: AMEinfo.com

Presence of major retail brands in Malaysia & Saudi Arabia

The following part of the report will compare the presence of few of the leading retail brands in Malaysia and Saudi Arabia. The no. of outlets, in some of the cases, has been described in brackets.

Table 4: shows the presence of some of the major retail brands in Malaysia and Saudi Arabia. Source: Mystore411.com and others

Policy

One of the key pillars for the growth of any industry in a country is policy and regulatory framework. An open and market oriented policy framework are more likely to stimulate growth and development in the long run. The following part of the report will compare Malaysia and Saudi Arabia across general business environment as well as policy framework pertaining to retail industry.

Retail business environment

General business environment

Saudi Arabian economy is marked by liberal economic policies and free market mechanisms stimulating foreign investments. The kingdom has biggest oil reserve outside Soviet Union and USA and like other Gulf counterparts, aim at diversifying its economy into industrial and service sector. The state generally does not interfere with the inflow and outflow of capital. It incentivizes businesses by providing favorable tax exempts, subsidies, provision of land at low price, exemption of custom duties on export etc. (Al A, 2007)

In line with Saudi Arabia, Malaysian economy is also marked with investor friendly business environment. During 1970s, when Malaysian economy was primarily based on mining and agriculture, govt. took diversification measures backed with centralized planning. During 70s to 90s, like other Asian Tigers, Malaysia recorded a strong economic growth. In the present time also govt. plays a pivotal role in the economy, but gradually it is reducing. One of the remarkable features of Malaysia economy is availability of easy credits.

Malaysia

The key elements of retail industry (especially pertaining to foreign investments) policies of Malaysia are as follows (MDTCC, 2010)

· Aims at modernization of the industry, ensuring growth of the local business at the same time

· All foreign involvements in retail sector, including; acquisition & merger, expansion, relocation, buying, taking over etc; require permission from Ministry of domestic trade, cooperative and consumerism (MTDCC).

· Work force should be reflective of over all racial composition of Malaysian population. It should ensure development of local inhabitants or Bumiputera.

· Regulatory framework for Hypermarket-minimum capital required is US $15.95 million (RM 50 million), at least 30% stake should be provided to Bumiputera within 3 years of incorporation, minimum floor space should be 5000 square meters and 30% of space needs to be allocated for Bumiputera SME product.

· Regulatory framework for Departmental store-minimum capital required is US $6.38 million (RM 20 million), and 30% of space needs to be allocated for Bumiputera SME product.

· Foreign investment is not allowed in the following- super market/ mini market (<3000 square meters), provision shop, convenience stores, fuel station with convenience stores, etc.

Saudi Arabia

The key elements of retail industry (especially pertaining to foreign investments) policies of Saudi Arabia are as follows:

· Retail being one of the few sectors, in Saudi Arabia, where 100 percent foreign ownership is not permitted. As per the guidelines, last revised in 2004, the maximum limit for foreign ownership in retail sector is 49 percentages.

· Any company in Saudi Arabia, with foreign investment, requires a foreign investment license.

· Franchising a popular concept used in the Kingdom. Franchise owners need to be local inhabitants and not 3rd party. Many of the leading retail brands such as Baskin Robins, McDonalds, and Burger King Etc operate in the Kingdom in franchise arrangement.

Tourism

Along with local inhabitants, tourism inflow also helps in boosting retail sales. Both Malaysia and Saudi Arabia are successful tourism destination. Religious pilgrimage is the key driver of Saudi tourism, whereas its Malaysian counterpart depends on exotic beachfront resorts, festivals and medical tourism. The following chart compares tourist inflow of Malaysia and Saudi Arabia.

Fig 5: compares the annual inflow of foreign tourists in millions, for Malaysia and Saudi Arabia. Source: Tourism Malaysia and Indexmundi.

Demographics

Demographic profile is one of the key drivers of the retail industry worldwide. A young, vibrant and well aware population ensures high spending on retail.

Table 5: compares Malaysia and Saudi Arabia across demographic parameters. Data are for the year 2010. Source: CIA World Fact book.

Transportation

A good transportation network, especially high volume of private motor vehicles, ensures the growth and development of out of town hyper markets. In the absence of motor vehicle people tend to visit nearby retail stores only.

A well developed transport and logistics network does not only help in sales but also ensures better functioning of big hyper market chains. In the absence of good logistic, big hypermarket chains are unlikely to import and circulate retail items in large volume, effectively.

Table 6: compares Malaysia and Saudi Arabia across transportation parameters (most recent by year). Source: nationmaster.com, numbeo.com

Conclusion

The report has compared Malaysia and Saudi Arabia across various parameters- economics, retail industry outlook, policy frame work, tourism, demographics and transportation. As discussed earlier, both the nations offer a great case to study. They have their own share of agreements as well as disagreements. Some of the key conclusions drawn are as follows:

· In both the countries, retail sector is important constituent of the national GDP and is witnessing high annual growth. The high growth of the retail sector is fuelled by higher disposable income, high percentages of youth and vibrant tourism sectors.

· Malaysia is considered as a high middle income country, where as Saudi Arabia, on account of high oil and natural gas reserve, is one of the rich nations in the world. Marked with high per capita income, it is a more fertile ground for luxury retail.

· Both are luring big retail brands to operate in their country. Saudi Arabia is a better destination than Malaysia in terms of a number of ease of doing business parameters such as – dealing with construction permit, getting electricity, registering property, taxation etc. Malaysia’s strength lies in the easy credits and high FDI in retail; 70 % against, 49 % in Saudi Arabia

· Malaysia has better infrastructure, logistic as well as telecommunication infrastructure, both considered as a backbone for developing a vibrant retail sector. Saudi Arabian strength lies in availability of gasoline at dirt cheap price and high availability of electricity.

Reference

1> RECON, 2008, Malaysia: a gateway to South East Asia,